Buying your first home is an exciting, yet sometimes intimidating venture. There are 3 major myths that I see potential first-time homebuyers make over and over again. So, I wrote this blog to help spare you the same heartache!

Myth 1: It’s too big of a risk

A house is an investment, and every investment comes with a measure of risk. Many people wait to buy a home because they have a short-term rather than a long-term view of money. Let me explain.

People will walk into an electronics store and think nothing of putting $1,500 on credit to buy a flat-screen TV. However, when I challenge them to put $5,000 or $6,000 down to buy a $200,000 house, they say, “I’m not going to get into debt.” Yet, the minute they walk out of the store carrying that ginormous TV, its value depreciates. In a matter of months, it will be worth significantly less than what they paid for it.

Buying a home is a great investment because its value will appreciate. Appreciation is simply the increase in an asset’s value over time. Here’s a secret–your home itself typically won’t appreciate over time, but the land it sits on will. The population will increase and, consequently, so will the demand for land. The result will be a higher property value than you originally paid for.

If the market happens to be at a point where your house would sell for less than what you paid for it, simply ride out the cycle. It will go up again–that’s why they call it a cycle. If possible for your situation, you can stay in the property until it’s a good time to sell. Or, you can quite easily rent out the property while you live in another space. This is called buy and hold real estate. The tenants will continue to pay the mortgage on your old place through their rent (you can even make a little more cash), and then you’re free to move where you please.

Myth 2: A downpayment is the only required financing.

Many young people will save religiously for a downpayment only to find that their finances have fallen short. It is true that you need to save between 3.5% (for FHA loans) and 20 percent for a downpayment (put more down if you can–this will get you a lower interest rate and allow you to pay off the home quicker.) However, there are other financing costs that will come back to bite you if you don’t save for them beforehand.

Here’s the cost breakdown:

Near or at the Time of Home Purchase:

- Down Payment: 3.5%-20% of House Cost (More if you can afford it!)

- Earnest Money: 1-3% of the purchase price of the home. The purpose is to protect the seller if the buyer backs out. If all goes well, this money is typically applied to the down payment or closing costs.

- Closing Costs: 1-3% of the home’s purchase price

- Moving Costs: Dependent on the buyer’s condition

Consecutive Monthly Payments:

- Principle, Interest, Taxes, Insurance, and Homeowner’s Association Fees: This should be no more than 25% of your monthly take-home pay.

- Emergency Fund: Money set aside in case something breaks or needs renovation. The recommended amount is 1% of your home’s value per year.

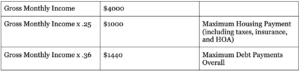

Key tip: Know how much house you can afford before you start looking. Typically, you want your monthly mortgage payment to stay under 25% of your take-home income. This protects you from becoming house poor (putting all your spare income toward your mortgage!)

In addition, before you qualify for a mortgage, lenders will obtain verification of your employment and income. They like to see at least two years of employment history as well as a debt-to-income ratio of less than 36%. Your debt-to-income ratio is how much of your monthly income you put towards debts: mortgage, car payment, student loans, credit cards, etc.

Several things can cause someone’s cost of living to unexpectedly increase. That’s why lenders like to see a good bit of wiggle room in your budget. You can use the following chart to calculate the maximum debt you should be acquiring in order to meet the requirements of your mortgage lender.

Myth 3: A shorter mortgage (15-year versus 30-year) is better.

A mortgage is a loan you take out in order to purchase a home. How long it will take you to pay off the debt on your house depends on two factors: what type of mortgage you get and how often you make payments.

Every mortgage payment contains principle and interest. Principle is the amount that goes towards the real value of your home, and interest goes toward your loan. Therefore, you want to do what you can to minimize the amount of interest you pay.

There are several types of mortgages, but for the purposes of this blog, I am going to discuss 15 and 30-year fixed-rate mortgages. Essentially, fixed-rate mortgages will lock you into a consistent interest rate that won’t change with the market. These are generally a better option.

Now, a 15-year mortgage will have a higher monthly payment, but it will be paid off quicker (in 15 years) and more money will go toward the principle. There is simply less time for interest to accrue. A 30-year mortgage will have a lower monthly payment, but it will be paid off slower and have more interest.

Many first-time homebuyers take this to mean that they should opt for a shorter mortgage. However, it is typically better to opt for a 30-year fixed-rate mortgage and make additional payments. This gives you more flexibility. If you pay off the 30-year mortgage in 15 years by making additional payments, you cut out even more interest. And, you have more flexibility in your budget if you need to pay less one month. Check out this amortization calculator to see what I mean!

If you have any questions about becoming a homeowner, please do not hesitate to ask us. We love your comments! And, if you know someone who wants to buy their first home in the next couple of years or so, please share this information with them.