The end of the year is always a great time to reconsider your financial goals. However, it’s important to contextualize them in light of the current economy. In America, consumer prices are estimated to have risen around 7 percent in 2022 alone (which seems like a very modest projection). We are in recessionary territory, and interest rates will continue to increase as long as inflation continues.

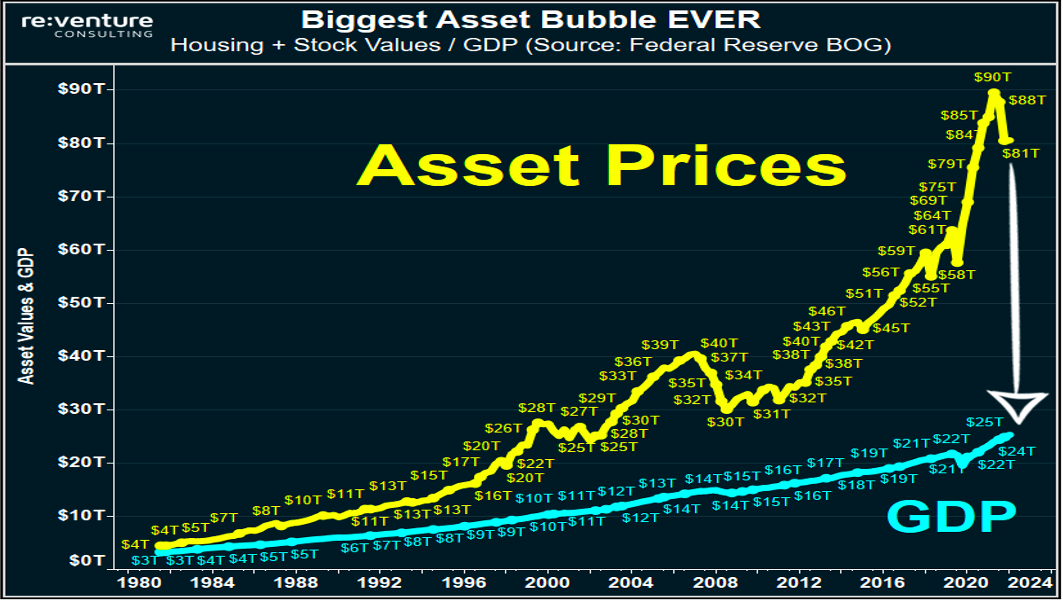

The chart below shows that asset prices have risen at a significantly higher rate than the GDP since 1980. As the gap widens, it will take more of your income to purchase assets. Inflation is high, and assets are in a bubble.

So, the following end-of-year financial checklist is a mixture of conventional and contextual wisdom. You will learn how to adjust your budget, position your assets, protect your credit, and save on taxes in the year to come. With practical wisdom and an ear to hear God’s direction, 2023 will be a year of growth for you.

End-of-Year Financial Checklist

1. Pause and listen for direction from the Holy Spirit

Everything we have belongs to God, and He is the ultimate source of wisdom when it comes to creating financial goals. The first part of partnering with God is pausing to pray before any creative process–and yes, building wealth is creative! There are so many different routes you can take with your finances this year, and God will give you practical peace about which direction to go. Examine your motivations for building wealth, submit to the pace of grace, and don’t try to knock down doors that aren’t ready yet.

2. Is your budget adjusted for inflation?

A good budget depends on knowing how much you earn and how much you spend. Thanks to inflation, your expenses have undoubtedly increased. Has your budget kept pace? Are you still allotting $100 a week for groceries but really spending closer to $200? Revisit your figures and see if there’s more room to save. Consider moving your emergency fund to a high-yield savings account if you haven’t already. An annual inflation rate hovering around 7 percent turns $1000 to $930 within a year. Currently, many banks offer a 4 percent return, which helps you save more dollars from being eaten up by inflation.

3. Do your investment strategies make sense in this economic environment?

The wisdom of Wall Street will tell you to invest 60% in stocks, 40% in bonds, and ride out the lows. However, I recommend diversifying even more, especially in hard assets that are more recession- and inflation-proof. As King Solomon said, “Divide your investments among many places, for you do not know what risks might lie ahead.” (Ecclesiastes 11:2) If you have big money, farmland and art are great places to spread out your wealth. For the average investor, hard assets like gold, silver, and real estate are stable yet lucrative options.

4. Do Your Real Estate Research

Is 2023 your year to buy a personal home or investment property(s)? If so, solidify your financial plan. Will you save for the down payment or use home equity? Wise financial stewardship advises using no more than 28% of your household income on a mortgage payment and no more than 36% of your debt. Scout out potential neighborhoods and ensure they fit the formulas:

- Properties are no more than 3-4x the median household income

- Rents can return 1-1.5% of the purchase price

- You can cash flow at least $300.

Housing prices will start to go down when the psychology changes. In many markets, prices are softening, but marginally because people are still in a housing bubble mindset. As the Fed continues to raise interest rates to combat inflation, fewer people will be able to afford a home, and prices should soften.

5. Order Your Credit Reports

A crucial component of any financial checklist involves staying on top of your credit score–especially if you plan to invest in real estate! A good score can significantly improve your interest rate, thus giving you access to cheaper money. Order a free credit report from the three credit reporting bureaus: Equifax, Experian, and TransUnion. According to The Federal Trade Commission, 79% of credit reports have errors. So, review your report for accuracy, including personal details, credit inquiries, credit cards and loans, cosigners, and collections data.

To learn more about your credit score, check out this blog.

6. Make Charitable Giving Tax Deductions

Generous giving has several benefits. First and foremost, when we give, we act like our heavenly Father. Financial giving is a great way to love our neighbor and partner with others to make a difference. Plus, charitable donations to qualified organizations give you a tax write-off! You have until December 31, 2022, to be eligible for a 2022 tax deduction. If giving is an important part of your financial checklist, you should do it by the end of the year!

I hope this blog has helped you formulate financial goals for the short and long term. Please write in the comments if you have additional tips or questions.

Make WealthBuilders a Part of Your Year-End Giving Strategy

WealthBuilders is a registered 501(c)(3). Free faith-based financial content such as this blog, webinars, podcasts, and more are made possible by our generous partners and donors. In 2022, we reached every country on the globe with biblically-based teaching on investing, business, real estate, and leadership! If WealthBuilders has blessed you this year, please consider giving a tax-deductible gift. You can give a one-time donation or partner on a recurring basis here.

Awsome info and straight to the point. I don’t know if this is in fact the best place to ask but do you guys have any thoughts on where to get some professional writers? Thx 🙂