As you I’m sure you know from your trips to the grocery store and gas pump, we are experiencing heavy inflation. It’s important to know how to appropriately steward your finances in accordance with the economic times. There are several great ways to invest during inflationary periods, but the one I want to talk to you about today is real estate investing. In this article, you will learn how to not overpay for a house regardless of the market. In addition, I will share the formulas I use to ensure my investment property financing is profitable.

The Current Real Estate Market

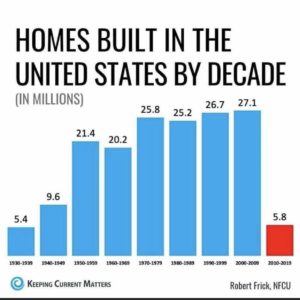

Right now, we are in a perfect storm for housing. Interest rates are low, the money supply is high, and housing supply is low. Whenever you have low interest rates and a high money supply, the value of hard assets will rise. So, if you have any investment in real estate right now, you are in a good position. On top of that, building rates from the past ten years are way lower than they have been in previous decades.

So, the demand for real estate is obviously high. However, that doesn’t mean that you have to settle and overpay for a property. Nor does it mean that you have to compromise on your investment property financing. If you follow these three steps, you can make a profitable buy and hold real estate investment.

How to Not Overpay for a House (Investment Property Financing Tips)

1. Check Local Rental Rates for Similar Properties

Before you purchase an investment property, it’s important to know how much it will rent for. You want to be sure that you can cover your principle, interest, taxes, insurance, management (PITIM) and any homeowner’s association fees from your tenant’s rent. This step is as simple as a thorough Google search. Type ‘Average rental rates in _______’ and be sure you’re paying attention to the specific location as well as the number of bedrooms and bathrooms. It is also helpful to research ‘Vacancy rates in ______’ to assess how strong the rental demand is in that area.

For example, let’s say you were going to buy an apartment/condo for an investment property in Denver. You would research and find that the average rent is $1,877 (varying by size of the property and the neighborhood where it’s located.) The vacancy rate is below average at 3.8%, which indicates that you have a pretty good chance of getting a tenant.

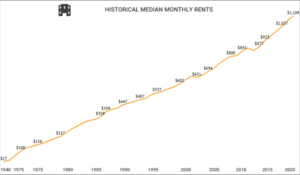

The great thing about rental rates is that they typically continue to trend upwards despite what the economy does. If less people can afford to own homes, they will rent. People have to live somewhere! Here is a chart depicting the historical median monthly rents in the United States since 1940. It shows that from 2000-2020, average rents rose from $602 to $1,104.

2. Calculate Cash Flow

Personally, I try to get at least $300 in positive cash flow from each of my investment properties. This ensures that you are building capital for your next investment and that you have enough to fund any necessary repairs. Calculate your cash flow by subtracting your entire monthly payment (including PITIM) from the average rental rate in that area. If possible, I also try to negotiate properties down to no more than 80% of what they’re worth. That’s a little harder in a seller’s market, but you can work with your realtor to see what’s feasible. That way you’re protected on the actual value of the home AND the cash flow side.

Let’s stick with our Denver example. If we can charge $1,877 for rent, we would need to land investment property financing for around $1,500 after PITIM. That’s possible, especially with interest rates as low as they are today.

3. Ensure Rent Will Pay at least .5% of the Property Value

This is another way of thinking about the previous step. This percentage used to be 1%, but the market and inflation make that nearly impossible. So, if you are going to charge $1,877 in rent for an apartment in Denver, aim for properties that are no more than $375,400 ($375,000 x .005 = $1,877.) However, you will want to verify that your mortgage with PITIM isn’t more than what you charge for rent!

I hope that these tips have given you confidence that you can get profitable investment property financing whether you’re in a seller’s market, an inflationary period, or both. Here’s the key—at some point, all things return to their real value. So, if something doesn’t have intrinsic value, you need to be careful about putting your money into it. That’s why I love investing in real estate—it’s real! It has intrinsic value, appreciates in the long-run, and continually provides positive cash flow (if you invest wisely!)

If you would like more guidance on how to invest in real estate, I recommend tuning into our WealthBuilders Real Estate Workshop Livestream. The in-person workshop sold out, but you can still join us virtually April 22-24, 2022, and view the content for three weeks after the event. For a limited time the Livestream price is $299—click here to learn more and register!